Sideways inheritance: how to stop your children being accidentally disinherited

Sideways inheritance can cut your children out of your estate. Learn how wills and trusts can protect your family. Practical, UK‑specific guidance.

Sideways inheritance: how to stop your children being accidentally disinherited

Sideways inheritance sounds like jargon. It isn’t. It’s one of the most common ways children are accidentally cut out of an estate.

It usually appears years after a death, quietly, through remarriage, new wills, or intestacy rules. By the time anyone realises, it’s too late.

This is preventable. But only if you plan for it on purpose.

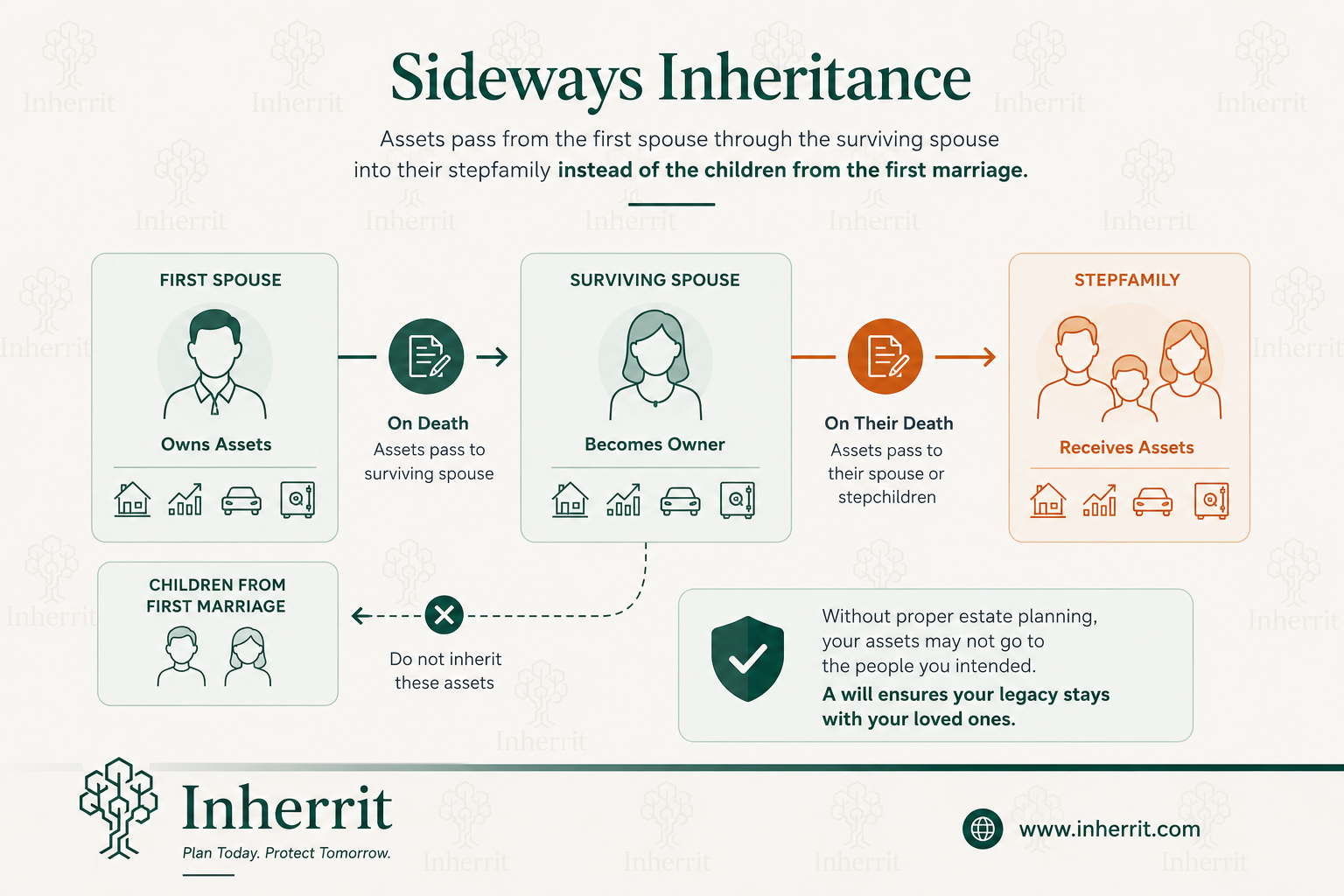

What is sideways inheritance?

Sideways inheritance (often called sideways disinheritance) is where assets that you expected to pass down your family line end up going sideways into another family instead.

Classic pattern:

- You leave everything to your spouse or partner.

- They later remarry or change their will.

- On their death, the combined estate passes to their new partner or that partner’s children.

- Your own children receive little or nothing from what you originally built.

Legally, nothing “wrong” has happened. Under the Wills Act 1837, any adult with capacity can change their will at any time. There is no obligation to keep a promise made to a late spouse about leaving assets to particular children.

That’s the sting in the tail: good intentions are not binding law.

How does sideways inheritance actually happen in England & Wales?

Let’s make this concrete.

1. Mirror wills and remarriage

Most married couples sign simple mirror wills:

“I leave everything to my spouse, and if they die before me, then to our children equally.”

On first death this works fine. The survivor inherits outright.

The problem starts later:

- The survivor remarries; under s.18 Wills Act 1837, that marriage normally revokes their existing will.

- If they die without making a new will, the intestacy rules apply and priority goes to the new spouse, not your children.

- If they do make a new will, they are free to favour their new partner and that partner’s family instead of your children.

Either way, what you left them can be redirected sideways very easily.

2. Intestacy after second marriages or new relationships

If someone dies without a valid will in England & Wales, the intestacy rules on gov.uk apply.

As at 2024:

- A surviving spouse/civil partner takes all personal chattels,

- Plus a statutory legacy of £322,000,

- Plus half of anything above that,

- Children share the remaining half above £322,000.

In blended families this is messy: - Childless second spouse inherits heavily,

- On their later death their will (or intestacy) controls where those assets go,

- Which may be entirely towards their own bloodline.

Your side of the family fades out over a generation or two.

3. Divorce, old wills and forgotten updates

Another very common pattern:

- Couple make mirror wills leaving everything to each other then children.

- They later divorce.

- One never updates their will but then remarries someone else.

- That remarriage revokes the old will altogether under s.18 Wills Act 1837.

- On death, everything passes under intestacy to the new spouse and then on again via their choices or intestacy position.

The original children get nothing from that parent’s estate despite what was once written down years earlier.

So sideways inheritance isn’t theoretical. It’s built into how English succession law works if you don’t put guard rails in place.

Where does HMRC and Inheritance Tax fit into sideways inheritance?

Sideways inheritance is mainly about who gets what. But tax shapes how people structure things in the first place, so we need to look at it briefly.

Under the Inheritance Tax Act 1984:

- Each person has a £325,000 nil‑rate band (frozen until April 2028).

- There is usually an extra residence nil‑rate band (up to £175,000) if you leave a home to direct descendants and meet certain conditions (HMRC guidance).

- Anything left outright to a UK‑domiciled spouse/civil partner is exempt from IHT (the “spouse exemption”).

Because of that last point, many couples feel pushed towards “everything to each other” wills for tax reasons. That structure maximises use of allowances between spouses but also maximises exposure to sideways inheritance risk later on.

The good news: you can often use life interest trusts and similar structures and still secure both IHT efficiency and protection for children. You do not have to choose between tax planning and protecting your bloodline if it is drafted properly under the Trustee Act 1925 framework and current HMRC practice.

The human side: a typical sideways inheritance scenario

Picture this:

- David and Sarah own a house worth £500,000 and savings/investments worth £200,000 in England.

- They have two children together: Emma and Jack.

- They sign basic mirror wills leaving everything to each other then equally to Emma and Jack.

David dies first: - Sarah inherits everything outright: £700,000 total estate value at that time (no IHT due because of spouse exemption).

- A few years later she meets Mark and remarries him; her old will is revoked by marriage automatically.

- She never writes another one; busy life, blended family dynamics, difficult conversations postponed “for another day”.

Sarah dies without a will:

- Intestacy rules kick in for her now larger estate (say it has grown to £800,000).

- Mark gets personal chattels plus £322,000 plus half of the remaining £478,000 = total around £561,000,

- Emma and Jack share only c.£239,000 between them – from both parents’ lifetimes’ work – while Mark now controls most of what was originally David’s wealth as well as Sarah’s own growth since his arrival on the scene.

- When Mark later dies his own children inherit his estate under his will/intestacy; Emma and Jack usually see nothing more from that pot.

That sideways step cannot be fixed afterwards by “challenging” anything unless there are very unusual facts such as lack of capacity or undue influence. In practice there usually aren’t; it’s just how the law works if nobody planned ahead properly.

How Scotland and Northern Ireland differ on sideways inheritance risk

The basic risk exists UK‑wide but some legal details differ by jurisdiction:

Scotland

Scotland has strong legal rights for spouses/civil partners and children over moveable estate (cash, investments etc.), regardless of what a will says. Heritable property (land/buildings) sits outside legal rights but is still part of overall planning.

So even if you try to cut out a child entirely in Scotland they may still claim legal rights against moveables; however houses can still shift sideways through remarriage or poor planning unless trusts or liferent arrangements are used sensibly within Scots law rules on liferents and special destinations.

Northern Ireland

in Northern Ireland succession law broadly mirrors England & Wales on intestacy structures and revocation by marriage/civil partnership; there are some differences in terminology and court procedure but not enough to remove sideways risk without using trusts or specific gifts in wills drafted with NI law in mind.

in short: wherever you live in the UK, relying purely on “everything to my spouse” is optimistic at best if you care about where assets land two relationships down the line.

Legal tools that actually prevent sideways inheritance

Here are the arrangements that work in real life rather than just sounding clever on paper:

1. Life interest trust (interest in possession trust)

a life interest trust inside your will lets you split two ideas cleanly:

a) who can use an asset during their lifetime;

b) who should ultimately own it when they die or move into care/sell up etc.

typical use with a family home under English law:

– Your half share of the house goes into trust on your death;

– Your spouse has a right to live there for life (or until remarriage/ cohabitation/ moving into care – depending how we draft it);

– They may also receive income from investments placed in trust;

– But they never own those assets outright;

– On their death (or earlier trigger), capital passes automatically to your chosen beneficiaries – usually your children – regardless of what is written in your spouse’s later will or who they’ve married since you died.

Used correctly this structure still normally qualifies for spousal exemption for IHT under IHTA 1984 because it counts as an immediate post-death interest for a spouse; so we keep tax efficiency whilst ring‑fencing capital from sideways drift.

2. Discretionary trusts

Where families are complicated – estranged adult child here, vulnerable beneficiary there – discretionary trusts give trustees flexibility instead of fixed entitlements:

– You create a trust in your will;

– Name a class of potential beneficiaries (e.g. “my spouse, my children and remoter issue”);

– Leave detailed guidance in a letter of wishes;

– Trustees decide who gets what and when based on circumstances over time rather than predictions made decades earlier.

For sideways inheritance this matters because trustees do not have to follow whatever new partner enters the picture; their job under Trustee Act 1925 duties is to act for all beneficiaries fairly rather than pleasing one surviving spouse who may wish everything redirected elsewhere.

There are IHT complications with discretionary trusts – especially around ten-year charges – so these must be designed carefully around actual asset values rather than thrown into every cheap online will template by default.

3. Specific gifts outright

Sometimes simplicity wins: leave some things directly where you want them now rather than hoping someone else passes them on voluntarily later:

– Gift part of your ISA portfolio straight to adult children;

– Leave defined cash sums (“pecuniary legacies”) before residue goes anywhere;

– Give personal items with sentimental weight directly down your line rather than through spouses who might later drift away emotionally from stepchildren.

This doesn’t solve every problem but it reduces how much can ever move sideways afterwards.

4. Avoiding mutual wills traps

People sometimes hear about “mutual wills” as an answer: both spouses sign wills promising never to change them after one dies.

In practice these arrangements often cause more litigation than they avoid.

They rely heavily on equity imposing constructive trusts after death; they sit awkwardly alongside changing tax rules; they’re inflexible if circumstances change radically.

My blunt view: use properly drafted life interest / discretionary trusts instead.

Mutual wills should be rare edge-case tools used only with specialist advice.

Sideways inheritance meets social care fees and creditors

There is another angle people rarely think about until crisis hits.

If you leave everything outright to your spouse:

– Their entire enlarged estate may be assessed for means-tested care under the Care Act 2014 framework;

– If they go bankrupt or face creditor claims later in life those inherited assets are fully exposed;

– On divorce from a second partner inherited wealth may form part of matrimonial pot subject to sharing orders.

If instead part passes into trust:

– Capital ring-fenced correctly inside certain types of trust is generally less exposed both for care assessment purposes and creditor issues (though local authorities do scrutinise “deliberate deprivation” cases hard);

– Your chosen beneficiaries retain ultimate entitlement even if life becomes financially messy for your surviving partner.

This isn’t about dodging responsibilities; it’s about not having an entire lifetime’s saving swallowed simply because legal structures were too naive.

Where digital organisation helps: avoiding practical sideways loss

Sideways loss doesn’t only happen through remarriage or bad drafting.

sometimes assets simply vanish because nobody knows they exist.

savings accounts forgotten, premium bonds untraced, a small pension scheme never claimed.HMRC holds billions in unclaimed estates across various institutions over time.

Tools like Inherrit help here:

you keep an encrypted inventory of bank accounts,pensions,policies,property details,even cryptocurrency wallets,alongside copies of your will,trust documents,and contact details for executors/solicitors.

executors then know what exists,so fewer assets fall through cracks or drift into bona vacantia territory by neglect rather than intention.

rather than trying to remember every account every few years,you update one secure hub when something changes.

💡 Pro tip: You’ve read about sideways inheritance. Now take the next step — our app helps you store your will, insurance policies, property deeds, and key contacts in one secure place, ready for when your family needs them.